The Hardest Thing for Early Stage NC Startups: Finding the Elusive 'Lead' Investor.

In this article, we dig into THE most common challenge fundraising, dig into why and provide strategies for finding your lead.

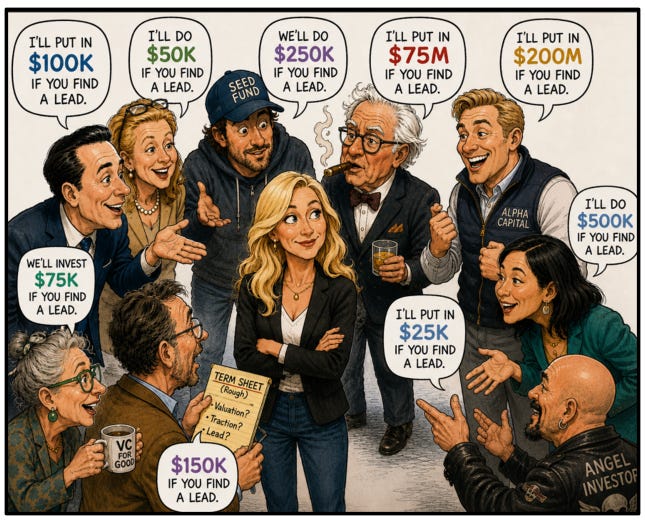

In the last 90 days, I’ve talked to at least 10 founders who have the exact problem illustrated above. They could raise their 1X-2X their pre-seed or seed round amount based on “I’d put in $X if you had a lead” - add those together and you’re there! But sadly it doesn’t work that way. You have to find that lead.

BUT FIRST!